Build-to-Rent Isn’t the Problem

The system incentivizing it is.

People are right to be angry when corporations get rich not from building housing, but from simply holding the land underneath it. They’re right that land value flowing to Wall Street instead of working families is a problem. We should solve these problems by addressing the systems that create them.

For a brief moment a couple of weeks ago, lawmakers who rarely agree on anything found common ground when the Senate passed the 21st Century ROAD to Housing Act by an 89-10 margin (easy explainer of its provisions). The bill itself is mostly good, but one provision targeting build-to-rent housing is still causing a significant fight. Under Title IX, any investor owning 350 or more single-family homes would be required to sell newly built rental homes within seven years.

The logic is politically intuitive: Wall Street has become a villain in the housing story, and the provision polls well across both parties.

The provision targets the corporate form of the developer, not the underlying dynamic that produces the problem. The concern of build-to-rent development exists because America has a land crisis as public institutions have systematically failed to capture the value their own investments create, leaving private actors to step into the gap and extract it instead. Restricting who can hold that land doesn’t change the dynamic. It just changes who benefits from it.

The families who would have rented those homes still need to live somewhere. The land value created by growing metros keeps flowing to whoever holds the title, whether that’s a pension-backed Real Estate Investment Trust or a local speculator sitting on an empty lot.

Meanwhile, The debate the provision ignited was real.

Over 100 housing groups — including Pew, the Mortgage Bankers Association, and the National Apartment Association — have signed letters in support of the bill but against the Build-to-Rent (BTR) provision. The establishment viewpoint is that BTR is necessary additional supply at a time when we are dealing with a severe housing shortage.

Here’s my take: strip the BTR provision, pass the rest, and ask the harder question: why do large private firms keep doing a better job of coordinating land development than the public institutions that are supposed to be doing it?

What build-to-rent actually is

Build-to-rent communities are purpose-built single-family rental neighborhoods designed from the outset to be rented rather than sold. They typically involve multiple actors: a master developer who assembles significant parcels of land on the suburban fringe, entitles it, and builds out community infrastructure; a BTR operator who acquires a designated parcel within that master plan; and a contracted homebuilder who constructs the actual homes. Some developments are more integrated than others. The BTR operator then retains ownership of the entire parcel, collecting rents from families who want the single-family experience without the commitment of a mortgage.

As Matt Stoller documented in his piece on the homebuilder industry, large homebuilders like D.R. Horton have increasingly become land financiers more than builders — acquiring cheap land on the urban fringe, holding it while it appreciates, then hiring subcontractors to build on it. BTR operators take this one step further: rather than selling finished homes, they retain ownership indefinitely, capturing not just the development margin but all subsequent appreciation.

Why hold rather than sell? Two structural advantages make the model uniquely attractive to institutional investors. The first is diversification: a BTR firm owning homes across the Sun Belt carries risk spread across dozens of markets in a way no individual homeowner can match. The second is capital access. Since 2008, institutional investors have retained uninterrupted access to cheap debt markets that have effectively closed to middle-income buyers.

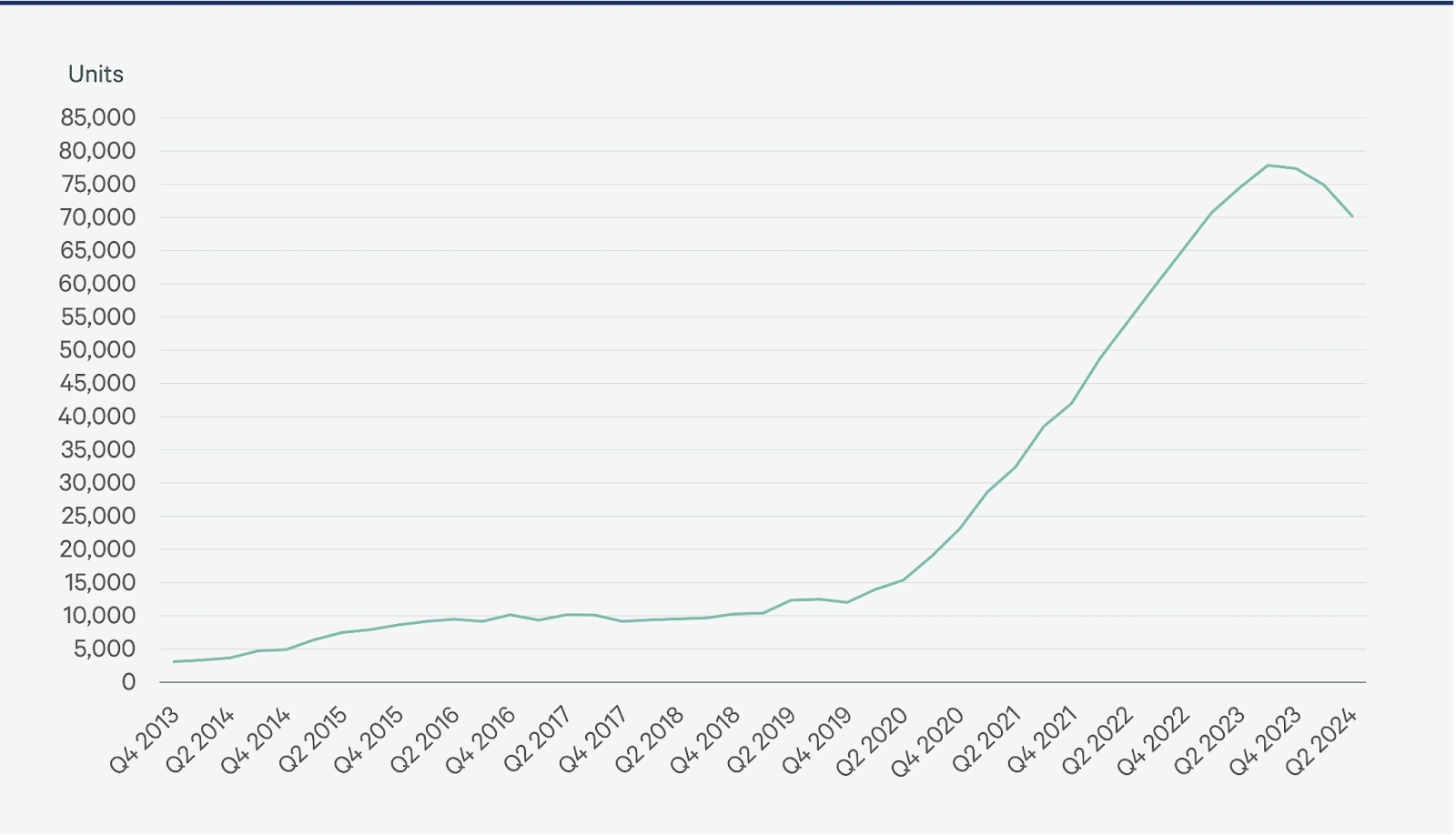

BTR currently accounts for somewhere between 3 and 10 percent of new single-family housing starts and has been one of the fastest-growing segments of new residential construction. The Pew Charitable Trusts estimated it adds between 70,000 and 130,000 homes annually to the housing supply. Industry groups argued, credibly, that the Senate’s seven-year disposal requirement would make the financial model unworkable.

None of that means BTR is above criticism. These firms are accumulating substantial wealth through land ownership, extracting rent from families who might prefer to own, and in some cases engaging in the kinds of fee-gouging and lease manipulation the FTC found at Invitation Homes. The moral discomfort is real. However, before we reflexively reach for the bonesaw, let’s understand what this symptom is telling us about the real disease it stems from – America’s land crisis.

The housing crisis is a land crisis

The deeper story here starts with something we’ve written about before: The Housing Crisis as a Land Crisis.

In most American cities, land near jobs, transit, and amenities is scarce and increasingly expensive. Zoning constrains what can be built on it. Infrastructure expansion is slow and politically contentious. When land values rise faster than wages, people’s incomes are extracted by high rents. And when land near the urban core is expensive and underbuilt, development pressure moves outward in search of cheaper land at the suburban fringe. This outward pressure is what generates most new housing supply in America today.

One of the reasons cities fail to develop their interior land — the vacant lots, the surface parking, the underutilized parcels next to transit stations — is that there’s no pressure on the owners of that land to do anything with it. Land sitting idle near a growing urban center appreciates in value simply because the city around it is growing. The landowner doesn’t need to build, doesn’t need to improve, doesn’t need to take any risk. They just wait, and the surrounding community’s investment in itself — in schools, transit, parks, public safety — flows into private land values as an unearned windfall. Development pressure then sprawls outward, not inward.

Conor Dougherty made this point compellingly–and controversially–in the New York Times: infill is slow, expensive, and politically blocked in most cities, while greenfield development on the edge offers scale and speed.

BTR in practice: the Cadence at Gateway example

This is a plot of land on the eastern fringe of Mesa, Arizona in 2018. It’s empty. Desert scrub, virtually worthless. But notice what’s right next to it: the Loop 202 San Tan Freeway and State Route 24, a major highway interchange built with public dollars that connected this previously remote corner of the East Valley to Phoenix’s employment corridors. That freeway didn’t just move traffic. It created land value. Suddenly this empty desert was thirty minutes from major employers, the Phoenix-Mesa Gateway Airport, Apple, Boeing, Intel. The land is now worth something, not because of anything the landowner did, but because the public built a road.

Harvard Investments and GTIS Partners foresaw that. In 2015 they announced plans for Cadence at Gateway, a 444-acre master-planned community on what had been the GM Desert Proving Grounds. Harvard and GTIS bought the land, did the planning and entitlement work, and built a community from scratch: 13 parks, 12 miles of trails, an 8-acre amenity hub with resort-style pools, fitness center, tennis courts, a café, and an event lawn, plus a new elementary school and retail at the main entrance. By 2020, Cadence had sold all 2,200 of its for-sale residential lots to national homebuilders — Lennar, Pulte, Toll Brothers, David Weekley, Maracay — at prices that reflected the community infrastructure already in place.

And then there is the small area highlighted in blue: Tricon Gateway, a 197-home build-to-rent community that GTIS developed inside the same master plan it co-owned, financed through a joint venture with the Arizona State Retirement System. The homes were built by a contracted homebuilder. Tricon Residential manages and owns every one of them. Tricon’s residents pay rent, use Cadence’s parks and trails, and walk to the same retail strip that Lennar and Toll Brothers buyers use. The BTR community is roughly 9% of the community’s residential units — a designated parcel within a larger master plan, not a standalone project.

This structure matters for the current policy debate. When Senator Warren’s provision requires investors to sell BTR homes within seven years, it doesn’t necessarily eliminate the housing on those parcels. In a community like Cadence, the master developer may simply sell that parcel to a homebuilder instead, who builds and sells individual units to buyers. Some of the backlash from housing advocates worried about supply may be overstated in that sense. Though, based on some anecdotal poking around Google, more recent build-to-rent projects appear to be more fully integrated (where the land owner and developer is the same as the house developer and landlord).

But Cadence also illustrates the deeper dynamic that produces BTR in the first place: the BTR operator benefits freely from surrounding public infrastructure they didn’t pay for, then captures the land value created within its perimeter indefinitely.

Thesis 1: BTR is a symptom of untaxed land rents — and so is SFH sprawl

The reason people hate BTR is not complicated: when a corporation owns a home and you rent it, the land value appreciation flows to the corporation. When you own the home yourself, it flows to you. The populist case against BTR is essentially an argument for widening access to asset ownership and keeping the housing wealth ladder accessible to more Americans. Everyone loves the housing ladder… as long as they get to climb it first. We have previously covered the contradictions for everyone excluded from it here:

It’s worth asking a harder question. We have built an economy in which the primary mechanism for middle-class wealth accumulation is owning land. That is a fragile and inequitable foundation. It produces winners and losers based largely on when and where people were born. The question should not only be how we get more people onto the housing wealth ladder. It should also be why so much wealth is stored in land in the first place.

When land rents are untaxed, two things happen.

First, landowners near urban centers have no incentive to develop. They can hold indefinitely while the surrounding city creates value for them. Surface parking lots sit blocks from transit stations. Vacant lots remain vacant for decades. This is the predictable result of a system in which holding vacant land in a growing city is a lucrative and low-risk investment. Sprawl is not just a planning failure. It is a tax policy failure.

Second, developers who build at the fringe create new land value where none existed, and BTR operators are uniquely positioned to capture it. The Loop 202 freeway made Cadence possible. Mesa’s schools make it desirable. BTR developers capture the value of the public investment as well as the private land value improvements indefinitely.

Thesis 2: Private sprawl developers capture created land value, and cities should learn from them

What BTR operators are doing within their property lines is a narrow but genuine version of land-value coordination: they hold ownership long enough to capture the value their investment creates. That is exactly what cities chronically fail to do.

Cities invest in transit, roads, schools, and parks. Each investment creates land value for nearby private landowners, value the landowners didn’t earn and that cities recapture only partially, through property taxes that lag market values, overtax buildings, and undertax land. The result is that cities chronically under-invest in themselves while the gains flow to whoever holds land nearby.

The actor closest to doing what cities should do is the master developer: assembling land, building infrastructure, capturing the resulting value. But they capture it once and exit. From digging through examples of recent build-to-rent communities, it seems integrated projects are becoming more common: the same folks creating the roads and plots are the ones developing and renting the homes. They understand they can capture the land value indefinitely.

What cities should be doing is the same thing. A city that captured a meaningful share of the value its investments create could reinvest it in more infrastructure, which would create more value, which would fund more investment. The mechanism is well understood: land value taxation or long-term ground leases. The political will to use them aggressively is what is almost always missing.

Where that leaves us

The housing groups that signed the letter opposing the BTR provision aren’t doing it because they think America should be a nation of renters. They’re doing it because they understand that in our current land system, BTR is one of the few mechanisms actually building new supply at scale in places where housing demand is real and growing. Killing it without a replacement mechanism doesn’t solve the land problem. It just removes one of the few private actors stepping into the gap that public institutions have left.

That doesn’t make BTR above criticism. The wealth accumulation happening through privatized land ownership is real. Tricon’s 2021 SEC filing recorded hundreds of millions of dollars in fair value gains on rental properties, not from building or improving homes, but simply from owning land in markets where the housing shortage kept getting worse.

What would actually change the dynamics is changing how we treat land value in the first place: not as an untaxed private windfall, but as something that reflects the collective investment of the community around it and should be substantially recaptured to fund more of that investment. Cities that invest in themselves create land value. If they captured much more of that value, they could invest more, which would create more value, which would fund more investment. We would be focused more on developing in our urban cores where the value of land is treated as a public good.

The ROAD to Housing Act is a good bill. Strip the BTR provision and pass the rest.

Greg Miller is Co-Founder of the Center for Land Economics.

A Georgist based third party would kick ass - with housing affordability being a cross party huge issue; Georgist have fact based analysis and solutions that the American cirizen would like, while the duopoly barely understand root causes let alone presenting solutions. Candidate (G) let's make them happen!

Another reason why BTR can have greater long-run value is the owners are likely to pursue upzoning in the future. NIMBY homeowners would not. This creates a wedge where the value of the assembled land is higher to developers than splitting it among NIMBYs.

If developers could trust city planners to be YIMBY the wedge wouldn't exist.