A German State Quietly Implemented a Land Value Tax

In Baden-Württemberg, a quiet reform shows land value taxation isn’t just theory—it’s already happening.

In 2025, Baden-Württemberg – a German state of 11 million residents – implemented a land value tax. Instead of taxing both land and buildings, it taxes land value alone. The experience is still young and the tax rate still small, but it sets a precedent: land value taxes are not politically impossible.

While the reform technically took effect last year, its passage was surprisingly quiet. I first heard about it through a forwarded email months after the fact. This is one of the largest contemporary implementations of a land value tax anywhere in the world, in a major industrial economy.

It deserves more attention.

Why this matters

Baden-Württemberg isn’t a small pilot program or a single city trying something unusual. It’s one of Germany’s largest and most economically important states — home to Stuttgart, major manufacturing hubs, and a mix of dense urban areas, suburbs, and rural regions. In other words, it’s a real economy with real land markets. That makes it an important and interesting contemporary example of a land-based property tax in practice.

The federal decision

Germany’s property tax, the Grundsteuer (literally: ground + tax), was based on ancient property valuations; in West Germany, assessments dated back to 1964 and in parts of East Germany, they went back even further, to 1935. (This is also the experience of some counties in the United States, particularly those for which regular reassessments are not mandated).

Over time, this created obvious distortions. Two similar properties in the same city could face very different tax bills simply because one had been assessed more recently or because local markets had evolved differently since the last valuation.

Eventually, the issue made its way to Germany’s Federal Constitutional Court. In 2018, the court ruled the entire system unconstitutional. Not because property taxes themselves were a problem, but because the way they were calculated violated a core constitutional principle: equal treatment under the law.

The court forced lawmakers to fix the system. If two properties are similar in reality, they should be taxed similarly. A system built on decades-old values couldn’t meet that standard anymore. The mismatch between assessed values and actual market conditions had simply become too large.

What followed was a compromise. The federal government designed a new framework for the property tax which crucially allowed individual states to opt out and create their own models. This became known in Germany as Grundsteuerreform (literally: ground + tax + reform – compounding words should be more common in the US).

That decision opened the door for local experimentation.

The man who saw it coming

Long before Baden-Württemberg adopted a land value tax, Dr. Dirk Löhr was helping lay the groundwork for one.

Löhr is a Professor of Taxation at the Trier University of Applied Sciences and, by his own description, a Land Value Tax proponent. He doesn’t present himself as a political operator or activist. In conversation, he comes across as methodical and understated, even a bit reluctant to take credit. But over the past decade, he has been one of the central figures behind Germany’s land value tax push.

Dirk Löhr participated in a Henry George School of Social Science panel.

He is not the kind of academic who is content to sit back and write papers. In 2012, years before the Federal Constitutional Court forced Germany’s hand, Löhr co-founded—alongside Ulrich Kriese of NABU, a German nature conservation organization—Grundsteuer: Zeitgemäß! (”Property Tax: Contemporary!”), an initiative built specifically around the coming property tax fight. The name was deliberate: the campaign positioned land value taxation not as a radical idea, but as a sensible modernization whose time had arrived.

“We knew,” Löhr told me, “it is a question of time that the constitutional court will say [property tax valuations were] unconstitutional.”

When the court finally ruled the property taxes were unconstitutional in 2018, Löhr and his colleagues were ready.

From there, the campaign assembled an unusually broad coalition: environmental groups, tenant advocates, researchers, urban planners, and local officials. The point was not to build a narrow ideological camp. It was to show that taxing land more intelligently could appeal to very different constituencies for very different reasons.

“Land value tax is not something left or right,” Löhr said. “There are some people on the left who like it and some people who are more right who also like it. And these people you can bring together at one table.”

After the federal court decision, they worked everywhere trying to get land value taxes into all states. The message landed best in the German state of Baden-Württemberg.

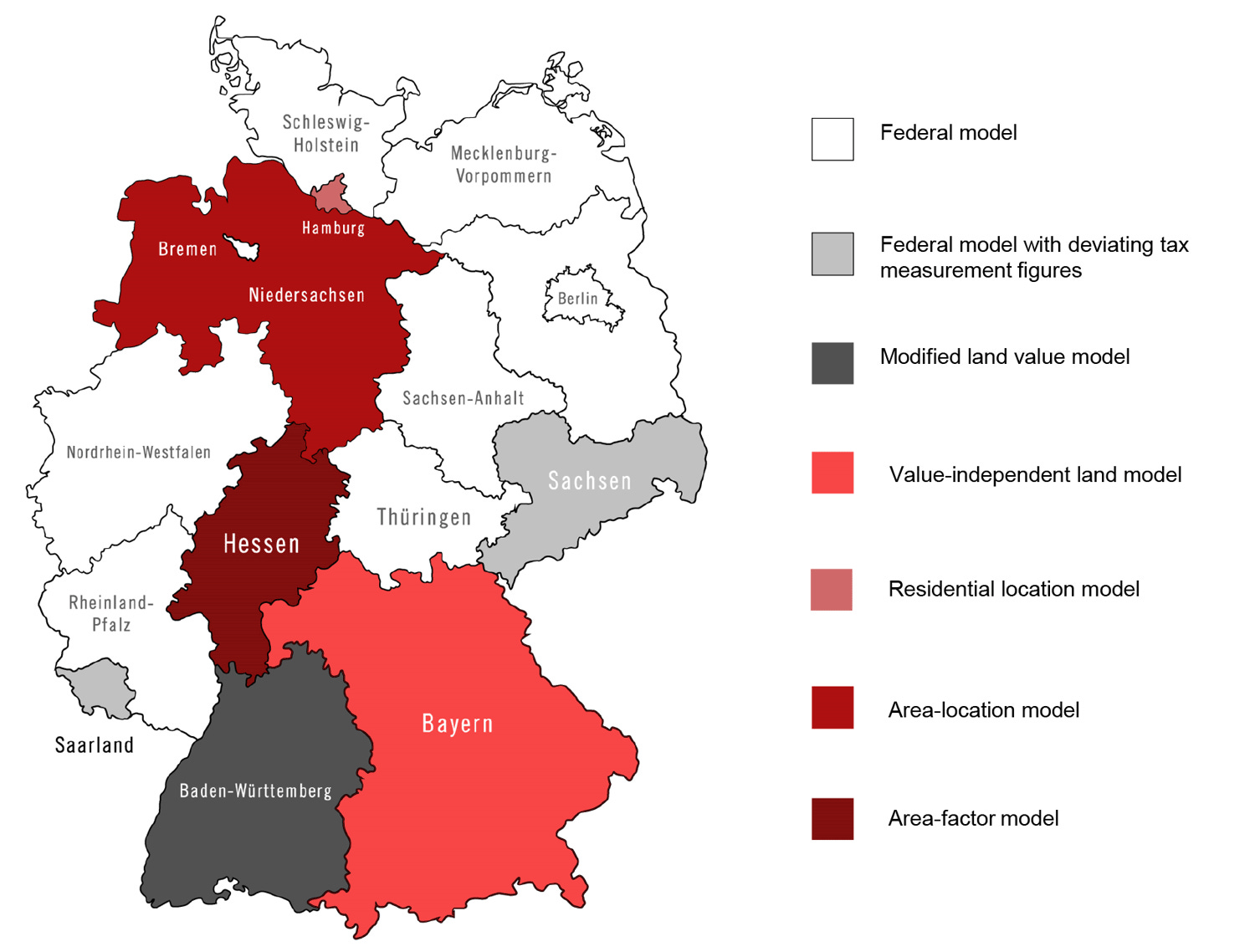

Baden-Württemberg

Most states chose to stick fairly close to the federal model, updating property values but keeping the same basic structure intact. Property taxes as normal.

Baden-Württemberg took a different path.

The state is governed by a coalition of the Green Party and the conservative CDU, and the Greens were the decisive factor. The land value tax fit naturally with their priorities—not because Löhr is a Green Party partisan, but because the policy logic aligned: “The Green Party found it very appealing because the land value tax is a tax which gives an incentive to be careful with the scarce resource of land.”

The tax aligned with green goals around compact development and land efficiency in ways that a standard property tax reform simply didn’t.

Löhr is candid that political alignment was the hinge. “It was the Green Party in power there. [LVT] had the most sympathizers in the Green Party,” he says. When he looked at other states where the campaign also had support, the Greens were not strong enough to push it through. In Baden-Württemberg, they were.

The result: Baden-Württemberg opted out of the federal framework entirely. On January 1, 2025, the Grundsteuer there began taxing land value alone.

Löhr draws a broader lesson from the experience: in Germany at least, reform doesn’t magically come from within the political establishment. “From the political machine, from the political business, there comes nothing,” he told me. “You have to give pressure from outside.” The coalition he built was precisely that kind of outside pressure.

How the tax actually works — and what it charges

Germany calculates property taxes in a few steps, but the logic is straightforward once you break it down.

Start with the assessed value of the property, or for BW, the land.

That value is then multiplied by a small state-level rate called the Steuermesszahl (tax + measure + number). Think of this as a base tax rate set by the state.

Finally, municipalities apply their own multiplier, called the Hebesatz (lift + rate), which scales the tax up or down depending on the city.

So in simple terms:

Land value × state rate × local multiplier = final tax bill

Baden-Württemberg chose to tax land alone but built in one notable political accommodation: a split-rate structure. Housing land is taxed at a lower effective rate than commercial land. Löhr views this as an imperfect but necessary compromise.

“It should be the same rate,” he told me plainly. “But we have two rates. This was the condition, otherwise it would have been impossible to push it politically.”

In Baden-Württemberg, the state-level rate is very small by U.S. standards: about 0.13% of land value, reduced to about 0.091% for residential land. That number is then multiplied by the local Hebesatz.

In Stuttgart, the Hebesatz is 160%, meaning the base rate is multiplied by 1.6. That brings the effective tax rate to roughly:

~0.15% on residential land

~0.21% on non-residential land

These are very small effective tax rates compared to the United States. In many U.S. cities, total property tax rates are often 1% to 2% of total property value (land + buildings).

Assessments for tax purposes will be updated every seven years (though the public real estate assessment boards do their own independent valuations every two years). Löhr finds this maddening. He has personally asked the assessment boards why they bother with biennial valuations if they won’t flow through to tax bills for seven years, and has not received a satisfying answer.

For all its compromises, Baden-Württemberg represents a rare move toward land-based taxation. Most states, however, went in a different direction.

What if you taxed buildings more?

Bavaria decided to go in almost the opposite direction.

Rather than basing the tax on values at all, Bavaria adopted a pure area-based model: the tax is calculated according to the physical size of the land parcel and the building footprint, with no reference to market value whatsoever. A prime commercial site in central Munich and a field on the rural fringe pay on the same per-square-meter basis.

Löhr doesn’t hide his skepticism. “They only measure the size of the building and the land,” he explained about Bavaria’s system. “According to the size — no matter how old it is, no matter how valuable it is — they put the [same] tax on it.” From a Georgist perspective, this abandons the core logic of taxing land rent entirely.

The simultaneous parallel and differing paths chosen by German states is why Löhr, in a 2020 paper, calls the German experience a “living lab”.

What comes next: legal threats and political limits

The reform is not without its threats. Opponents, primarily real estate interests and a taxpayers’ association, have filed suits challenging the land value tax at both the state tax court and the federal tax court simultaneously. The plaintiffs’ argue against any method that involves valuation—even the federal model which they are also seeking to undo in other states.

Löhr, who has been tracking the case closely, has been called on to defend the reform’s methodology against hired experts brought in by the plaintiffs. A hearing is expected in autumn 2026.

The opponents preferred alternative is Bavaria’s area-based system: a flat tax on physical size with no reference to value whatsoever. It taxes property mainly by lot area plus building area/use, so a larger low-value parcel in rural areas can face a higher tax base than a smaller but much more valuable downtown property if the latter has less taxable area.

In reality, these are organizations with vested interests. They try to muddy the waters on any government regulations and taxes in order to protect the business interests they represent.

Even if the law survives the courts, the path to higher rates is constrained. German States control few taxes, mostly property and business. Most taxes are levied at the federal level, and states have limited access to federal tax levers like the value-added tax. Therefore, Baden-Württemberg does not have flexibility to lower other tax levies in exchange for raising the land value tax.

For now, the Green Party’s re-election in Baden-Württemberg’s most recent state elections means the reform is almost certainly safe for another four years. But expansion remains a harder fight than preservation.

The bigger picture

One of the world’s great skepticisms about land value taxation has always been political feasibility. Baden-Württemberg is a direct challenge to that skepticism. It required years of unglamorous coalition-building, a favorable constitutional moment, and the right political alignment in a single state. But it happened.

We will be watching what comes next in the courts, in the data, and in any other state or city that takes note. But none of that changes what has already been demonstrated. “If it is possible here… in sleepy Germany” Löhr says, “it should be possible anywhere.”

We are always looking to connect with folks who want to see LVT in their local area. Do you have leads on land value tax potential or want help with local efforts? Reach out greg@landeconomics.org.

Greg Miller is the Co-Founder and Executive Director of the Center for Land Economics.

Incredible! I was born in BaWü and had no clue this was going on.

Yes, the German Vice President for the International Union for Land Value Taxation, Professor Dirk Loehr, worked hard to build a coalition that resulted in the successful passage of legislation for land value tax in the German province of Baden Wurtenberg. See details here: https://theiu.org/land-value-tax-for-baden-wurtemberg-germany-with-dr-dirk-loehr/